As we prepare to welcome 2025, the term “inflation” has become increasingly familiar, dominating headlines and conversations over the past several years. While many people understand inflation as rising prices, fewer grasp how deeply it can influence major aspects of life—particularly the housing market. From mortgage rates to home prices and rental costs, inflation has a significant role in shaping the real estate landscape. In this article, we aim to demystify inflation, explore its causes, and examine how it impacts everyday life, including housing, one of the most critical sectors of the economy.

What Is Inflation?

So let’s kick things off with the basics, at its core, inflation refers to the sustained increase in the general price level of goods and services within an economy over time. Essentially, when inflation occurs, the purchasing power of money decreases. For example, a $20 bill might buy less a year from now than it does today because of rising prices.

Inflation is commonly measured as a percentage rate, representing how much prices have increased over a specific period. A simple way to conceptualize inflation is to think of it as the erosion of the value of money—as prices go up, your money buys less. This phenomenon is influenced by several factors, including production costs, demand for goods and services, and the availability of money in the economy.

As we just passed the holiday season, a striking example of inflation’s impact comes from a recent article in USA Today analyzing the grocery haul from the holiday classic Home Alone. In 1990, Kevin McCallister’s groceries totaled $19.83. Purchasing the same items in 2024 would cost $57.54, or $58.54 with Illinois sales tax. Even with a dollar-off coupon, the total represents a 190% price increase over 34 years. This stark contrast underscores how inflation affects everyday purchases and erodes the purchasing power of money over time.

- Half a gallon of milk: $1.89

- Half a gallon of OJ: $3.79

- Butternut large white bread: $2.89 (Wonder Bread not available)

- TV dinner: $3.99 (Stouffer’s classic meatloaf frozen meal)

- Frozen mac and cheese: $3.69

- Tide liquid detergent: $12.99

- Saran wrap: $2.99

- Bounce dryer sheets: $6.99 (120 count)

- Toilet paper: $8.39

- Toy soldiers (not available, so Amazon price listed): $7.49

Grocery list source: USA Today

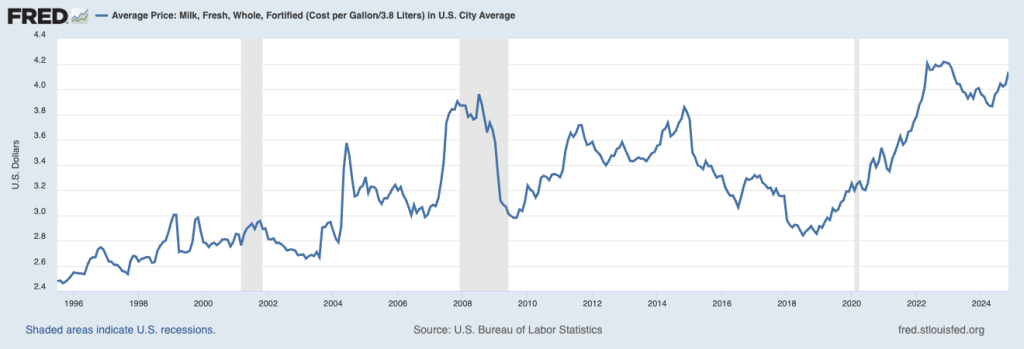

U.S. Bureau of Labor Statistics, Average Price: 1 Gallon Milk

Another illustrative example is the cost of milk, as shown by Federal Reserve Economic Data (FRED). In November 1990, the average price for a half-gallon of fresh, low-fat milk was $1.34. Fast forward to November 2024, and that same quantity of organic milk now averages $4.83. This dramatic price increase over 34 years highlights how inflation impacts even the most basic household staples. A FRED chart vividly depicts this steady rise, reinforcing the tangible effects of inflation on everyday items.

How Is Inflation Measured?

Economists use specific tools to gauge inflation, providing insights into how prices are changing over time. The most commonly used measures include the Consumer Price Index (CPI), the Gross Domestic Product (GDP) Deflator, and the Personal Consumption Expenditures (PCE) Price Index. Each of these measures provides a unique perspective on inflation’s effects across different sectors of the economy.

Consumer Price Index (CPI)

The CPI tracks the average change in prices that consumers pay for a standardized “basket” of goods and services. This measure focuses on goods purchased by households, including both domestic and imported products. The CPI is updated monthly and covers a wide range of consumer expenses, from food and clothing to healthcare and transportation. As one of the most widely recognized indicators of inflation, it often serves as the basis for cost-of-living adjustments in wages and Social Security benefits.

Gross Domestic Product (GDP) Deflator

Unlike the CPI, the GDP Deflator measures price changes for all goods and services produced domestically. It excludes imports and includes services, offering a broader perspective on inflation’s impact within an economy. The GDP Deflator reflects changes in both consumer and producer prices, making it particularly useful for analyzing overall economic trends. Because it encompasses the entire economy, the GDP Deflator can provide insights into inflation’s effects on sectors beyond consumer goods.

Personal Consumption Expenditures (PCE) Price Index

The PCE Price Index is another tool for measuring inflation, published by the Bureau of Economic Analysis. It measures changes in the prices of goods and services purchased by households, providing a comprehensive view of consumer spending patterns. Unlike the CPI, the PCE includes a broader range of expenditures, such as healthcare costs covered by employers or government programs. Because of its expansive scope, the PCE is often favored by policymakers, including the Federal Reserve, as a key measure of inflation.

Why Multiple Measures?

Each inflation measure serves a distinct purpose, and together they provide a more complete picture of price changes in an economy. For example, while the CPI offers valuable insights into consumer-level impacts, the GDP Deflator captures inflation affecting businesses and government spending. Similarly, the PCE Price Index provides a more holistic view of household consumption patterns, making it ideal for setting monetary policy. By examining these tools collectively, economists and policymakers can develop more nuanced strategies to address inflation’s challenges.

What Drives Inflation?

Economists have identified several primary drivers of inflation, each of which contributes to rising prices in distinct ways. Here, we’ll explore three main causes: the cost-push theory, the demand-pull theory, and the impact of increased money supply. However, real-world inflation often arises from a complex interplay of these factors, reflecting the dynamic nature of economic systems.

1. Cost-Push Inflation

Cost-push inflation occurs when the rising costs of production—such as materials, energy, or labor—lead businesses to increase the prices of their goods and services.

- Rising Production Costs: If the price of raw materials such as metals or agricultural products increases, companies face higher production expenses. To maintain profitability, they pass these costs on to consumers in the form of higher prices.

- Wage Increases: Higher wages, often resulting from union negotiations or shortages of skilled labor, can also push up production costs. For example, if workers successfully lobby for higher pay, businesses might respond by raising the prices of their products.

- Supply Chain Disruptions: External shocks, such as natural disasters or geopolitical conflicts, can disrupt the supply chain, driving up the costs of production and leading to inflation. The COVID-19 pandemic offers a recent example where supply shortages contributed to price increases across many sectors.

Examples of cost-push inflation are seen in events like the oil crises of the 1970s, where rising energy prices increased the cost of production across industries, ultimately leading to higher prices for consumers.

2. Demand-Pull Inflation

Demand-pull inflation arises when consumer demand for goods and services exceeds the available supply, leading businesses to raise prices to balance the scales.

- Increased Disposable Income: Tax cuts or other financial windfalls can leave consumers with more money to spend, driving demand for products that may not immediately see a corresponding increase in supply.

- Lower Interest Rates: When borrowing becomes cheaper due to reduced interest rates, consumers and businesses are more likely to spend, further increasing demand and pushing prices upward.

- Economic Booms: Periods of rapid economic growth, characterized by rising employment and consumer confidence, often lead to higher spending levels, which can outstrip the economy’s capacity to supply goods and services.

Demand-pull inflation often occurs during periods of economic growth. For instance, a booming economy with low unemployment can lead to higher consumer spending, outpacing production capacity and driving up prices.

3. Expansion of the Money Supply

When governments increase the amount of money circulating in an economy, it often leads to inflation. This can happen in two primary ways:

- Printing More Currency: Governments may produce more money to finance spending, but this dilutes the value of existing money, leading to inflation.

- Increased Borrowing: By taking on debt, governments can inject additional money into the economy, stimulating demand but also contributing to rising prices as supply struggles to keep up.

- Quantitative Easing (QE): Central banks may use QE policies to stimulate the economy by increasing money supply through the purchase of financial assets. While QE aims to boost investment and growth, it can also contribute to inflation if demand rises too quickly.

A classic example is the hyperinflation experienced in post-World War I Germany, where excessive printing of money led to a dramatic loss of value in the currency.

Interplay of Factors

In reality, inflation is rarely driven by a single factor. For example, a supply chain disruption might lead to cost-push inflation, while simultaneous government stimulus measures could amplify demand-pull effects. Understanding these interconnected dynamics is crucial for policymakers aiming to manage inflation effectively.

Built-In Inflation

Built-in inflation, also known as wage-price inflation, is a self-reinforcing cycle that occurs when businesses raise prices to cover rising costs, including wages, which then leads workers to demand higher pay. This expectation of future inflation perpetuates the cycle and can create sustained upward pressure on prices.

The Cycle of Wage and Price Increases

The essence of built-in inflation lies in its cyclical nature:

- Workers demand higher wages to keep up with rising costs of living.

- Businesses, faced with higher labor costs, raise the prices of goods and services to maintain profit margins.

- As prices rise, workers again seek higher wages to afford those goods and services, continuing the cycle.

Role of Expectations in Built-In Inflation

Expectations play a critical role in perpetuating built-in inflation. If businesses and consumers believe that inflation will continue, they adjust their behavior accordingly:

- Businesses preemptively raise prices in anticipation of higher costs.

- Workers push for wage increases to safeguard their purchasing power against expected future price hikes.

This “expectation effect” can lead to inflation becoming ingrained in the economy, making it more challenging to control.

Real-World Examples

One notable example of built-in inflation occurred during the 1970s, often referred to as the “Great Inflation.” During this period, persistent inflation led to widespread expectations of continued price increases. Workers consistently demanded higher wages, and businesses, expecting ongoing inflation, raised prices. This cycle contributed to prolonged high inflation rates that required aggressive monetary policies to break.

Controlling Built-In Inflation

Addressing built-in inflation requires targeted strategies:

- Monetary Policy: Central banks may raise interest rates to reduce demand and curb price increases.

- Wage Agreements: Governments or industry leaders might negotiate wage agreements to prevent excessive wage demands that exacerbate inflation.

By addressing the root causes of built-in inflation, policymakers aim to disrupt the wage-price spiral and stabilize the economy.

The Effects of Inflation

Inflation exerts widespread influence across various aspects of life and the economy, impacting both individuals and businesses in different ways. While moderate inflation can have positive effects, excessive inflation often brings significant challenges.

Positive Aspects

- Economic Growth: Moderate inflation, typically around 2%, encourages consumer spending. When consumers expect prices to rise slightly in the future, they are more likely to make purchases now, boosting demand and stimulating production.

- Debt Relief: Borrowers benefit from inflation as the real value of their debt decreases over time. This effect can ease financial burdens, especially for those with fixed-interest loans.

- Incentivized Investments: Inflation can make holding cash less attractive, prompting individuals and businesses to invest in assets like stocks, real estate, or commodities, which can drive economic activity.

Negative Effects

- Erosion of Purchasing Power: One of the most immediate effects of inflation is the reduction in the purchasing power of money. As prices rise, consumers find their income buys less, leading to financial strain.

- Impact on Savings: Inflation diminishes the real value of savings over time, particularly for those with funds in low-interest accounts that fail to keep pace with rising prices.

- Uncertainty and Reduced Investment: High and unpredictable inflation creates economic uncertainty, discouraging long-term investments by businesses and individuals.

- Inequality: Inflation disproportionately affects low-income households, which spend a larger portion of their income on necessities like food and housing. Rising costs in these areas hit these households the hardest.

Impact on Trade

- Export Competitiveness: Inflation can devalue a nation’s currency, making exports more competitive in global markets. While this can benefit exporters, it may lead to trade imbalances.

- Costlier Imports: A weaker currency increases the cost of imported goods, which can further drive inflation domestically, particularly in economies reliant on foreign products.

Hyperinflation: The Extreme Case

In rare but severe cases, inflation spirals out of control into hyperinflation, where prices increase at an exponential rate. Historical examples include Zimbabwe in the late 2000s and Germany during the Weimar Republic. Hyperinflation often leads to the collapse of monetary systems and requires drastic measures to restore economic stability.

By understanding both the benefits and challenges of inflation, individuals and policymakers can better navigate its effects and implement strategies to mitigate its negative impacts while leveraging its positive aspects.

Inflation and the Housing Market

Inflation has a profound impact on the housing market, influencing everything from home prices to mortgage rates.

Rising Home Prices

During periods of inflation, the cost of materials such as lumber, steel, and concrete tends to rise. These higher costs often lead to increased home prices as builders pass the expenses on to buyers. Additionally, as the purchasing power of money decreases, the nominal prices of homes often climb to keep pace with inflation. For instance, a house priced at $300,000 during low inflation could see its price rise significantly over a few years of high inflation, even if the actual value of the property in real terms remains relatively unchanged.

The rising costs of labor in construction also contribute to increasing home prices. With inflation pushing wages higher, builders and contractors must account for these additional expenses in their pricing, further driving up costs for homebuyers. This creates a challenging environment for first-time buyers or those with limited budgets.

Higher Mortgage Rates

To combat inflation, central banks often raise interest rates, which directly impacts mortgage rates. Higher borrowing costs make monthly payments more expensive for buyers, reducing affordability and slowing demand in the housing market. For example, a 1% increase in mortgage rates could add hundreds of dollars to a homeowner’s monthly payment, significantly affecting their purchasing power.

Higher mortgage rates also discourage homeowners from refinancing their existing loans or upgrading to larger properties. As a result, fewer transactions occur in the market, potentially leading to a cooling effect on home sales and slowing overall market activity.

Increased Rental Costs

Inflation affects the rental market in parallel ways. Landlords face rising costs, such as property maintenance, utilities, and property taxes, which they often pass on to tenants in the form of higher rents. This can make renting increasingly unaffordable for many individuals and families.

Additionally, as higher mortgage rates deter home purchases, more people turn to renting, driving up demand for rental properties. This increased competition in the rental market gives landlords greater leverage to raise rents further, exacerbating affordability challenges for tenants.

Real Estate as a Hedge Against Inflation

Despite these challenges, real estate remains a popular investment during periods of inflation. Property values tend to rise over time, often outpacing inflation, which helps protect investors’ purchasing power. Real estate also generates income through rental yields, providing a steady return even as prices climb.

Commercial real estate can be particularly advantageous in an inflationary environment. Long-term leases often include escalation clauses that allow landlords to increase rents in line with inflation, ensuring their income keeps pace with rising costs. For individual investors, owning property offers both a tangible asset and a potential safeguard against the eroding effects of inflation on cash savings.

Inflation’s Impact on Your Life

While inflation affects everyone differently, its effects are often less pronounced in the U.S. due to relatively stable rates over the past few decades. However, wage growth doesn’t always keep pace with inflation, leading to financial strain for some.

Who Benefits from Inflation?

- Borrowers: Inflation can reduce the real value of debt over time, benefiting those with fixed-rate loans. For example, if a borrower secures a 30-year fixed mortgage during a period of low interest rates, the inflationary rise in wages and prices over time diminishes the relative burden of their monthly payment, making their debt effectively cheaper.

- Businesses with Pricing Power: Companies able to adjust their prices effectively can maintain profit margins. For instance, businesses in sectors with high demand and few competitors may raise prices without losing customers, leveraging inflation to their advantage.

- Real Estate Investors: As property values and rental prices tend to rise with inflation, real estate can act as a hedge, preserving and even increasing the value of investments over time.

Who Suffers from Inflation?

- Savers: Inflation erodes the real value of savings, reducing purchasing power over time. Individuals who keep their money in low-interest accounts may find their savings worth less in terms of what they can buy as prices climb.

- Fixed-Income Earners: Those on fixed incomes, such as retirees, may struggle to keep up with rising costs. Even minor inflation can significantly impact their standard of living, as their income does not adjust to accommodate higher prices.

- Low-Income Households: Inflation disproportionately affects low-income households, which spend a larger portion of their income on essentials like food, housing, and utilities. Rising costs in these areas can strain already limited budgets, forcing difficult choices about spending priorities.

- Consumers: Inflation can lead to “sticker shock” for everyday goods and services, causing frustration and financial stress as wages fail to keep up with rising expenses.

Preparing for Inflation’s Impact

To mitigate the effects of inflation on personal finances, individuals can take proactive steps:

- Invest Wisely: Diversifying investments into inflation-resistant assets like real estate, commodities, or inflation-protected securities can help preserve wealth.

- Increase Financial Literacy: Understanding how inflation impacts various financial products and strategies can empower better decision-making.

- Review Budgets Regularly: Adjusting spending habits to prioritize essentials and reduce discretionary expenses can help offset rising costs.

- Consider Fixed-Rate Loans: Locking in lower interest rates on loans during periods of low inflation can provide long-term financial stability.

- Negotiate for Cost-of-Living Adjustments: Workers should advocate for wage increases that reflect inflationary trends to maintain their purchasing power.

Closing things off…

Understanding inflation helps demystify one of the most critical aspects of the economy. While it may not always be a pressing concern, knowing how inflation works and what drives it provides valuable context for financial decisions. Whether you’re a homeowner, renter, investor, or simply trying to navigate everyday expenses, being aware of inflation’s broad impact on life can help you prepare and adapt effectively to changing economic conditions.

{kind=link}